John Jerrim

Last week, I had the pleasure of speaking at the Sutton Trust summit about access to “high status” universities. It was great to be able to engage with a number of leading experts in higher education and widening participation over the two days. For the summit, I produced a report (pdf) outlining various issues surrounding widening access in England and the United States. These range from the link between family background and access to high status institutions, to the thorny matter of tuition fees, living costs, bursaries and debt.

Although the report seems to have been generally well received, it has also touched on some sensitive nerves. In particular, David Willetts, the minister for universities and science, stressed that no graduate has to pay back their loan until they earn more than £21,000 – and then only nine pence in the pound over this amount.

This is indeed an incredibly important point, as my colleague from the London School of Economics Gill Wyness pointed out during our session at the summit. Such “income contingent loans” help insure young people against the risk associated with investing in a degree, and mean they do not have to turn to wonga.com if they do not immediately find a well paid job.

However, one cannot escape the fact that at some point this debt has to be repaid. This is particularly relevant for young people attending elite institutions such as Oxford, Cambridge and the London School of Economics. Graduates from such leading universities tend to earn the highest wages. It therefore seems reasonable to ask, how much will attending one of these elite institutions costs?

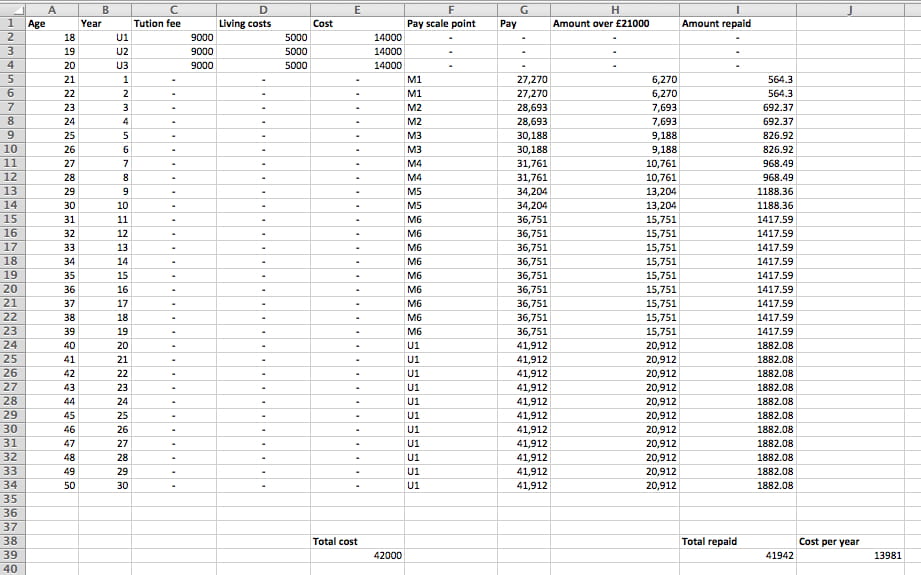

Unfortunately, this is not an easy question to answer, as it depends upon the specific career path chosen after university. But let’s take secondary school teaching as an interesting example. How much might an Oxbridge graduate who enters this noble profession pay for their degree?

Below is a spreadsheet with some back-of-an-envelope calculations based upon the following (generally conservative) simplifying assumptions:

- Zero real interest is paid on the loan and there is zero inflation

- There is no real pay increase in the teaching pay scales and no change to the £21,000 repayment threshold

- The debt is written off after 30 years (as per the current HE finance system)

- All costs associated with post-graduate study (including a PGCE) are ignored

- The teacher chooses to work in an inner-London school throughout their career

- They complete a 3-year undergraduate course

- They work full-time continuously between the ages of 21 and 50

- They take out a a £9000 tuition fee loan and a £5000 loan to cover living costs

- Their parents’ household income is roughly £40,000 per year

- The teacher is promoted bi-annually (from M1 to M6 on the teacher pay scale) during their first ten years of service. They then remain on pay point M6 for the next 10 years (to age 40) and then move on to pay point U1 to age 50[1].

Click on graphic to see a clearer version

To highlight a few key figures:

- This student (and prospective teacher) would accumulate a debt pile of around £42,000 by the end of their course.

- They would repay their debt at age 50, just before the 30 year cut-off point where the outstanding balance is written off

- The cost of their university education would therefore equal approximately £14,000 per year (including all tuition, books and living expenses).

This is of course just one single example. Many Oxbridge graduates will go on to enjoy much higher wages, incur substantial real interest on their debt, and will pay back substantially more. Others may decide to live outside of London, follow a different career path or work part-time, with university costing them substantially less.

However, one thing should be abundantly clear. Income contingency may mean that repayment of debt is manageable and reduces the financial risk of investing in a university degree. But for the majority of young people, the cost of attending one of England’s most prestigious universities is going to be quite high. Indeed, even more stark figures come from this cost calculator, which shows that even medium earnings graduates may make total repayments of more than £60,000.

Prospective students, as well as the Secretary of State, should remember this when thinking about higher education and the student finance system currently in place in England. They should be clear that going to a high status university is likely to cost quite a lot of money upon graduation. Furthermore, the Government must start to present figures for the total cost of higher education separately from the funding mechanisms (income contingent loans) that are designed to reduce risk and ease the upfront costs of attending such an institution.

You can find out more about John’s work at johnjerrim.com

Close

Close