Close

Close

Financial Literacy Part 4: Do disadvantaged children receive enough financial education in school?

By Blog Editor, on 11 February 2022

John Jerrim, UCL Social Research Institute

This blog post first appeared on the IOE blog.

In the third blog post in this series, I started to investigate socio-economic differences in the inputs into young people’s financial skills, focusing upon the role of parents.

Schools, of course, also have a key role in helping to develop children’s financial skills. Therefore, in this final blog of the series, we turn to socio-economic gaps in the provision of financial education within primary and secondary schools.

Big gaps in primary schools

Let’s start by looking at what happens in primary school. Figure 1 illustrates the percent of primary pupils who say they have been taught various financial skills at school, stratified by socio-economic background.

There are two striking results.

First, there are consistently large socio-economic gaps. For instance, children from advantaged socio-economic backgrounds are much more likely to report that they have been taught skills such as working out change from shopping (67% versus 54%), saving money (43% versus 28%), and the difference between the things you “need” and things you “want” to buy (36% versus 27%) than their disadvantaged peers.

Second, it is notable how only quite a small proportion of primary school children are taught some really key financial skills at school. For instance, even amongst higher socio-economic status families, only around one in five primary children are taught about bank accounts, how to keep track of spending and saving, and how to spot that advertising is trying to sell them something.

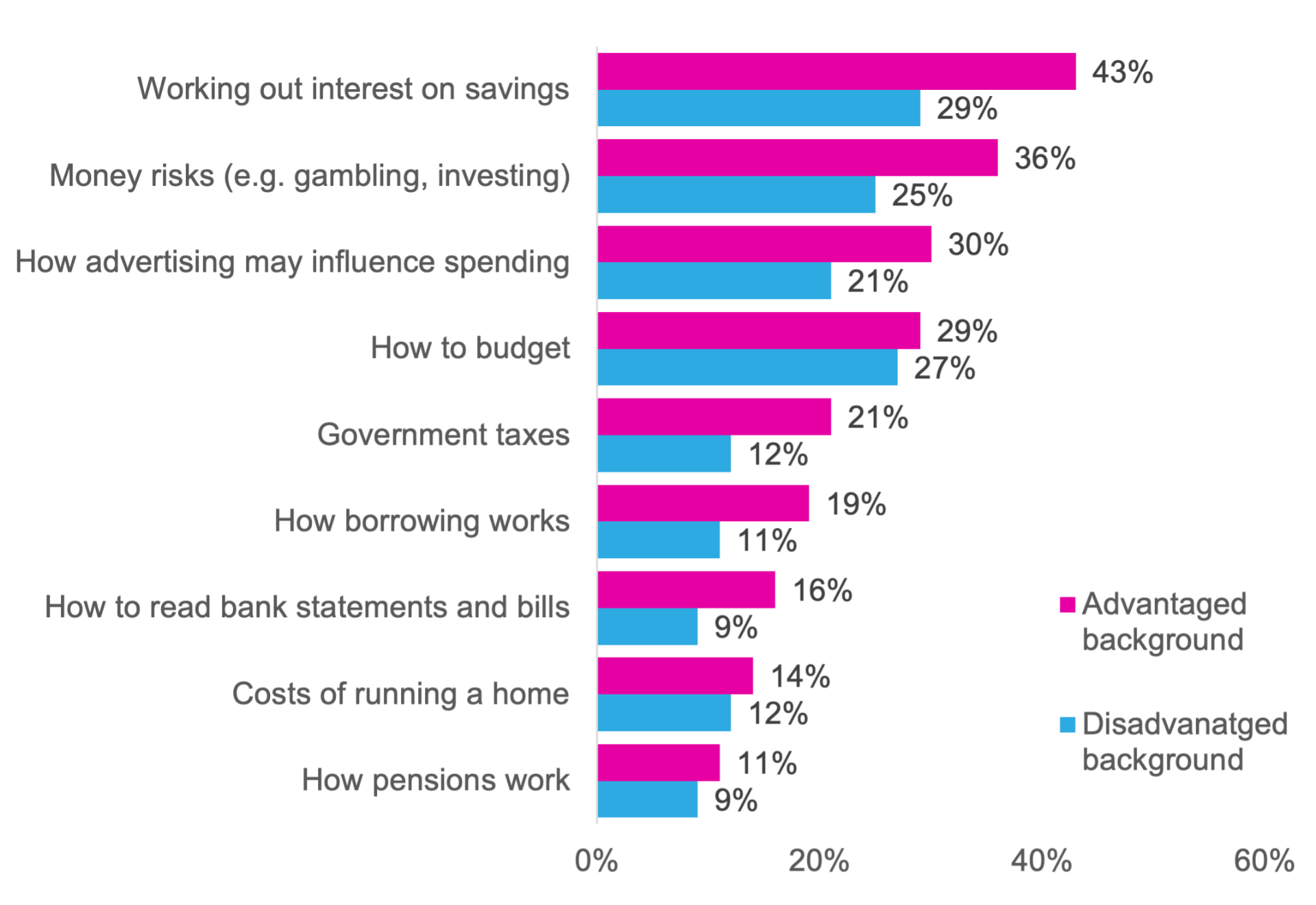

Interestingly, Figure 2 illustrates how a similar pattern emerges during secondary school as well. This presents the clearest evidence to date that the financial education provided to socio-economically advantaged and disadvantaged pupils differs significantly throughout their time at school. Moreover, some key basic financial life skills – such as learning how to budget, how to read bills, and understanding how borrowing works – are only taught by schools to a minority of disadvantaged pupils.

Figure 1. Socio-economic differences in the provision of financial education during primary school

Figure 2. Socio-economic differences in the provision of financial education during secondary school

With respect to the socio-economic gap in financial education provision during primary school, it is also notable how it seems to increase over time, between age 7 (end of Key Stage 1) and age 10 (nearing the end of Key Stage 2). This is illustrated in Figure 3, which combines responses to various questions into a scale, and reports changes in the socio-economic gap over time as an effective size.

In other words, while seven-year-olds from rich and poor backgrounds report receiving similar amounts of financial education at school, this gap in provision increases significantly during Key Stage 2.

Figure 3. Change in socio-economic status gap in “money planning” education provided to primary school pupils

Notes: “Money planning” includes topics such as saving, how to keep track of spending and saving, how to keep money safe and borrowing from banks.

Increase the focus of financial education in the school curriculum

The above suggests that greater time needs to be made in the school curriculum to provide financial education to young people – particularly those from lower socio-economic backgrounds.

Currently, only a minority of low-income children report receiving any education through their school in some key financial life skills. This puts them at a disadvantage compared to their more advantaged peers, with the gap in provision particularly pronounced towards the end of primary school.

One option could be to integrate financial education skills into the Key Stage 2 tests (with the most obvious choice being mathematics). This would provide schools with a clear incentive to ensure young people develop these vital life skills, which currently seem to be pushed out of the school curriculum.