Close

Close

Mobile Money & Elder Care from Kampala

By charlotte.hawkins.17, on 22 September 2019

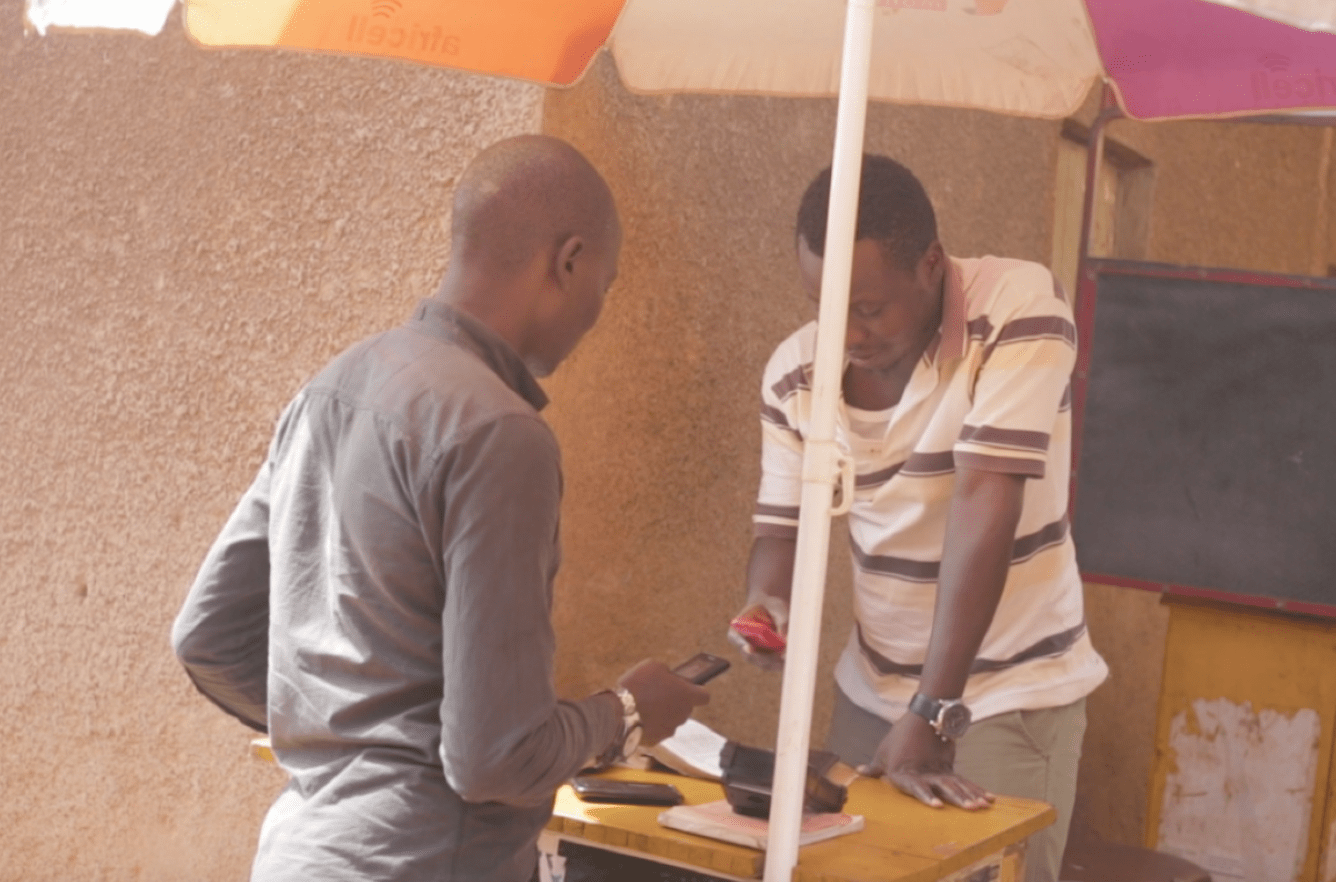

Calling and mobile money are the most ubiquitous uses of mobile phones in the Kampala fieldsite. This connects people to their relatives across distances, allowing people to check on family or request assistance. Mobile money is often lauded as an example of adapting technology to requirements ‘from below’ (Pype, K., 2017), offering financial flexibility and connection (Kusimba et al., 2016: 266; Maurer, 2012: 589). With 33 mobile money vendors in the low-income neighbourhood where fieldwork was conducted, it is the most convenient and accessible platform for saving and transferring money.

Various people in Lusozi explained how they provide for their parents and relatives in the village without visiting them as “you can send money on the phone”. People sending money take cash to an agent, who arranges the transfer to the recipient’s phone number via their mobile. Whilst relatives living in rural areas may be able to grow their own food, money is necessary for other amenities, transport, school fees, hospital bills, and burial costs. As one woman explained, if she wasn’t sending her parents money, they would have no other source of income; recently, her mother had a stomach ulcer, so she sent her money to go to hospital. And from the perspective of an elder in the village in Northern Uganda, “life’s easier now with phones”, as they are able to communicate family problems with relatives in the city and mobilise necessary funds. This also exacerbates the burden of care for urban relatives. A local councillor in Lusozi explained how he bought his sister in the village a smartphone in order to make communication easier between them. But he actually finds the connectivity has made life “a bit harder” for him, as it has increased his obligation; when people have problems, they can immediately let him know and he’s expected to find money for them. Before, news of a death could take a week to reach him, by which time he may have even missed the burial and the accompanying financial obligations.

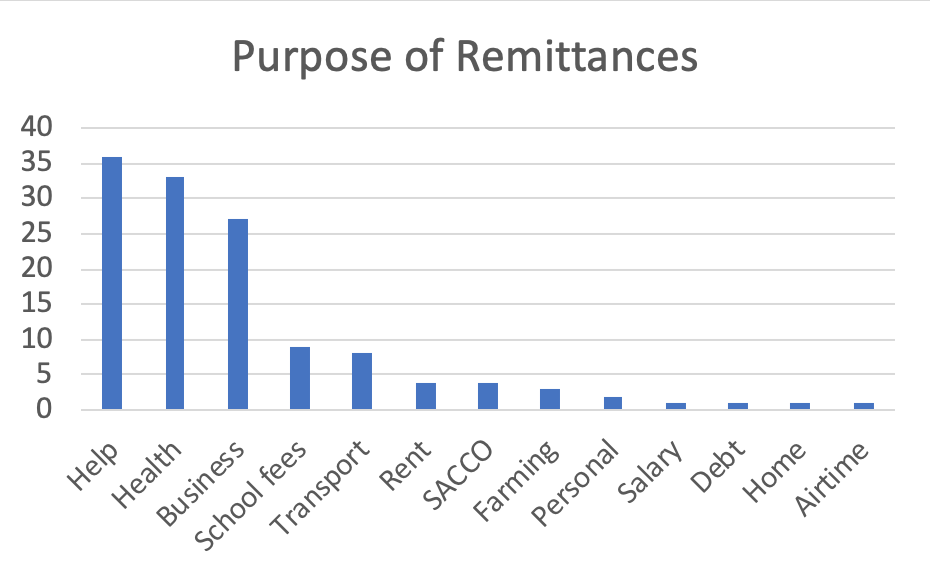

In a survey of 50 respondent’s phone use, only 3 people said they had not used mobile money in the past 6 months. Those who had used it sent and received money 3 times a month on average. We asked them about the last 3 times they had sent or received mobile money, who the person was, the amount and reason for remitting. Of 130 recorded remittances, the average amount sent was just over 200,000ugx, ranging from as little as 10,000 to 10,000,000ugx. Mostly, remittances were sent or received from siblings (28%), parents (12%), friends (11%), and customers (10%). Sometimes people had deposited money for themselves, using their phone as their bank. The greatest proportion of remittances (28%) were for ‘help’, which could include money for upkeep, food, ‘pocket money’ or gifts. This was followed by remittances for health purposes (25%), which could include hospital bills, medicine, transport to hospital and surgery costs. 6 of these transfers were received or forwarded by the respondent in a chain of remittances, for the purposes of supporting older relatives. For example, one respondent had received 200,000ugx from her daughter, in order to help her take her mother in the village to hospital; or another who received 30,000 from their Aunt for their grandmother’s hospital bills. Perhaps the older person was unable to receive the money themselves, or perhaps other relatives weren’t trusted to pass on the money.

As economic anthropologist Bill Maurer notes, mobile services such as mobile money are appropriated within existing communicative networks (2012: 593). These instances of phone use demonstrate how mobile phones can provide a platform for intergenerational care between the city and the village. This works against a pervasive academic, public and everyday discourse about the declining social position and experience of older people in Uganda and Africa more broadly (e.g. Nzabona and Ntozi: 2017; Nankwanga et al., 2013; Van Der Geest, 2011; Oppong, 2006; van der Geest, 1997), often associated with broader contextual shifts, such as the urbanisation and technologization which have necessitated and facilitated mobile money practices. Research participants often lamented the Westernisation, increasing materialism and individualism, of the younger ‘dotcom’ generation exposed to outside influences. But in these everyday instances, ‘dotcom’ technologies are also shown to up-hold family support and obligation towards older relatives, despite greater distances between them.

References:

- Kusimba, S., Yang, Y., Chawla, N., 2016. Hearthholds of mobile money in western Kenya: Hearthholds of mobile money in western Kenya. Econ. Anthropol. 3, 266–279. https://doi.org/10.1002/sea2.12055

- Maurer, B., 2012. Mobile Money: Communication, Consumption and Change in the Payments Space. J. Dev. Stud. 48, 589–604. https://doi.org/10.1080/00220388.2011.621944

- Nankwanga, A., Neema, S., Phillips, J., 2013. The Impact of HIV/AIDS on Older Persons in Uganda, in: Maharaj, P. (Ed.), Aging and Health in Africa. Springer US, Boston, MA, pp. 139–155. https://doi.org/10.1007/978-1-4419-8357-2_7

- Nzabona, A. and Ntozi, J. (2017) Does urban residence influence loneliness of older persons? Examining socio-demographic determinants in Uganda. Unpublished

- Oppong, C., 2006. Familial Roles and Social Transformations: Older Men and Women in Sub-Saharan Africa. Res. Aging 28, 654–668. https://doi.org/10.1177/0164027506291744

- Pype, K. (2017) ‘Smartness from Below’, in What do Science, Tehcnology and Innovation mean from Africa? eds Clapperton Chakanetsa Mavhunga. MIT Press

- Van der Geest, S., 1997. Between respect and reciprocity: managing old age in rural Ghana. South. Afr. J. Gerontol. 6, 20–25. https://doi.org/10.21504/sajg.v6i2.116