Close

Close

BP’s Energy Outlook 2035: betting on dangerous climate change

By ucqbndj, on 7 April 2014

Will humanity be collectively able to avert dangerous tipping points for climate change? Probably not, according to BP’s Energy Outlook 2035(1). Sadly, this may well be true. Is it good news for BP? Yes, rather so.

Is BP’s Energy Outlook 2035 an objective assessment of reality? Only to an extent.

BP Energy Outlook presents itself as a realistic assessment of reality, yet it is

- a reality that BP actively shapes and

- it creates a perception of reality that is beneficial to BP.

- It also wittingly or unwittingly aids the perception that industrialising countries are responsible for emissions reaching a level that makes dangerous climate change likely, thus generating a sense that climate action in OECD countries will only have a limited impact.

When presenting the BP Energy Outlook 2035 at University College London on 1st April 2014, BP’s Group Chief Economist and Vice President, Christof Rühl, left no doubt that he considers climate policy to be low on the agenda of policy makers. According to the Outlook climate change policies will remain too lax for staying within the emissions confines recommended by scientists: “Global CO2 emissions from energy use grow by 29% or 1.1% p.a. over the forecasting period. Policies to curb emissions continue to tighten, and the rate of growth of emissions declines, but emissions remain well above the path recommended by scientists.”(2)

What if climate policies would become stringent enough for staying within the 2 degree limit? Following HSBC 25% of BP’s proven and probable reserves would be ‘unburnable’ under a low carbon policy environment consistent with a scenario (‘450’), which limits global warming to 2C, with “BP’s value at risk from unburnable reserves [being] equivalent to only 6% of its market value as most of the ‘lost’ reserves are low margin (3,4). This doesn’t sound too bad. Yet BP is still investing into more exploration and extraction, ensuring that their interests continue to be pitted against the successful implementation of a low carbon regime with extensive coverage.

BP does’t just assess what would be the most likely future developments in energy markets, it also actively shapes them. According to BP its Outlook “is based on a “most likely” assessment of future policy trends (5). Is BP just responding to markets signals and expectations of regulatory developments? Past investments, “sunk costs”, mean that “oil companies are unlikely to stop extracting oil, even if they invest in renewable energy (6). If “exit” is not likely, “voice” is: lobbying and the shaping of perceptions. Standard economic approaches treat firms as solely responding to government intervention (7). Yet firms such as BP actively invest in politics (8,9). Big oil and energy intensive industries want a world with a low carbon price. Others, e.g. renewable energy companies, energy efficiency pioneers and the concerned public, want a high carbon price. What BP tells us in its Outlook is that they think they will win.

BP’s Energy Outlook creates a perception of reality that is beneficial to BP. BP is a publicly traded company. A threshold carbon price can benefit BP as oil and gas gain in desirability when coal’s higher carbon intensity drives it to the sidelines. While a carbon price high enough to stay within a tolerable degree of global warming would also hurt BP it would still hurt oil and gas companies far less than coal companies. BP could probably manage the transition. Its suggestions of substituting gas for coal in the mid-term make sense. However, for BP loosing 6% of its market value doesn’t sound like an enticing proposition. A scenario compatible with a reasonable likelihood of averting dangerous climate change threatens the profitability of BP’s assets. Acknowledging this would presumably not have the most benign effects on its share price. Concerning the argument that some of BP’s assets may prove to be unburnable, they write “we believe that the unburnable carbon approach to assessing the impact of potential climate regulation on a company’s value oversimplifies the complexity of the issue and overstates the potential financial impact (10). Creating an impression that the future will be benign for big oil may yet turn out to be delusional for investors at large but is still good for current shareholders. The situation could be overdetermined: BP may not have much of a reason to assume that stringent climate policies will be put in place. Yet, even if they had reason to assume it, it wouldn’t be in their interest to admit it. Currently, the markets don’t price in the risk that climate regulation stringent enough to ward off dangerous climate change could impact on fossil fuel companies’ share prices (11). If BP recognised a low carbon scenario in their outlook as a realistic possibility, it would raise the question of how such a scenario would impact on their assets, entertaining the prospect that some might become unburnable or “stranded”. This could change market perceptions, with some investments moving out of more and some into less carbon intensive forms of energy. If BP included the possible impacts of a low carbon scenario on market demand in its Outlook it would become apparent that BP is actively investing on the assumption that this is not going to realise — that they bet on a future that entails dangerous climate change.

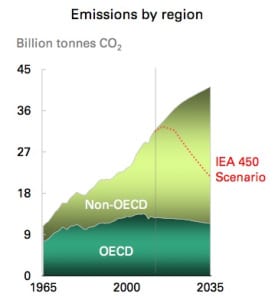

The Outlook can also be interpreted as suggesting that industrialising countries are responsible for emissions reaching a level that makes dangerous climate change likely. When commenting on Christof Rühl’s talk, environmental economist Paul Ekins, Professor of Resources and Environmental Policy and Director at the UCL Institute for Sustainable Resources, pointed out that the BP forecast graph depicting emissions by regions (see above) may be taken to suggest that the emissions cuts (compared to a baseline scenario) necessary for being in line with the International Energy Agency scenario “consistent with the goal of limiting the global increase in temperature to 2°C” (IEA 450 scenario) (12) would need to come from non-OECD developing countries. Yet, in order to make limiting emissions palatable for developing countries, OECD countries clearly need to take the lead.

Considering that the OECD member countries have a joint population of 1,257 million in 2012 (13), with the global population exceeding 7 billion (14), a mere stabilisation of OECD emissions seems hardly adequate. Differences in capabilities as well as historical responsibility clearly mandate a pioneering role in decarbonisation for industrialised countries. While lower demand from industrialised countries for fossil fuels makes them cheaper and thus raises incentives for industrialising countries to rely on them, lower prices also make future exploration and extraction efforts less attractive. As investment for renewables increases in industrialised countries, prices also fall for industrialising countries. It is far from clear that OECD countries’ climate action would be insufficient for remaining below the 2C target. Even if the target was exceeded, such action would be far from futile. If rich countries pioneer low carbon infrastructures, this will also help industrialising countries to rein in their appetite for fossil fuels.

The BP Energy Outlook 2035 suggests to solely give a realistic forecast (15). Yet BP forecasts a reality it helps to create. And its forecast further bolsters investments into this kind of reality. BP’s sense of realism is a confidence in its own prospects. While much can be learned from the data, the way it is presented supports fatalism, helps to keep up share prices and aims to provide legitimacy to further fossil fuel exploration and extraction. It provides the rationale for betting on dangerous climate change.

Nino Jordan, Doctoral Researcher, UCL ISR

Nino is a doctoral researcher at the UCL Institute for Sustainable Resources. His research focuses on business interests towards environmental regulation and the interactions between innovation and regulation.View Nino’s profile.

References

- BP (2014) BP Energy Outlook 2035.

- BP (2014) BP Energy Outlook 2035., p. 81

- HSBC Global Research (2013) Oil & carbon revisited. Value at risk from `unburnable’ reserves

- On “unburnable carbon” see also Carbon Tracker and the Grantham Research Institute on Climate Change and the Environment (2013) Unburnable carbon 2013: Wasted capital and stranded assets.

- BP (2014) BP Energy Outlook 2035., p. 95

- David Coen, Wyn Grant, and Graham Wilson (2010) Perspectives on business and government, David Coen, Wyn Grant, and Graham Wilson(eds.) The Oxford Handbook of Business and Government, Oxford University Press, Oxford, p. 18.

- “…economics has no use for a concept of power because it is assumed away in the conditions of the pure market.” Colin Crouch (2010) The global firm: The problem of the giant firm in democratic capitalism, David Coen, Wyn Grant, and Graham Wilson (eds. ) The Oxford Handbook of Business and Government, Oxford University Press, Oxford, p. 149.

- On firm “investment” in politics see Colin Crouch (2004) Post-democracy, Polity Press, Cambridge.

- On BP’s political contributions see e.g. Hiskes (2010) BP’s donations to Congress are more worrying than its donations to Obama

- BP (2014) BP Energy Outlook 2035., p. 14

- See Carbon Tracker and the Grantham Research Institute on Climate Change and the Environment (2013) Unburnable carbon 2013: Wasted capital and stranded assets.

- “A scenario presented in the World Energy Outlook that sets out an energy pathway consistent with the goal of limiting the global increase in temperature to 2°C by limiting concentration of greenhouse gases in the atmosphere to around 450 parts per million of CO2.” IEA Website

- http://data.worldbank.org/country/OED

- http://www.un.org/apps/news/story.asp?NewsID=45165

- Christof Rühl: “Don’t shoot the messenger!”, University College London on 1st April 2014