Close

Close

How to manage geopolitical risk and understand its implications on your portfolio and regional stability: Russia and the Ukrainian Crisis

By Lisa J Walters, on 23 March 2017

By Dr Eugene Nivorozhkin, Senior Lecturer in the Economics of Central – Eastern Europe

Centre for Comparative Studies of Emerging Economies

The economic and political turbulence around Russia in the aftermath of the Crimea annexation in March 2014 is an interesting illustration of how a geopolitical event is itself necessary but not sufficient to cause significant geopolitical risk for investment portfolios.

The Ukrainian crisis prompted a number of countries and international organisations to apply sanctions against individuals, businesses and officials from Russia. In addition to diplomatic actions, the measures included travel bans and freezing assets owned by Russian officials and friends of Putin. A broad set of measures targeted sectoral cooperation with Russia and more general economic matters. In particular, Russian state banks were excluded from raising long-term loans in international financial markets. Bans were implemented on arms deals and exports of dual-use equipment for military use. The EU/US ban included exports of selected oil industry technology and services, to name just a few.

The Russian equity market was heavily affected by the consequences of the country’s involvement in the political and security crisis in Ukraine. As of December 31, 2015, Morgan Stanley Capital International (MSCI) Russia index had a forward price/earnings (P/E) ratio of 5.41x, far below its historical average, and below 11.10x for MSCI Emerging Markets and 15.45x for MSCI AC World; and it was priced on a price-to-book (P/B) basis at 0.62x, compared to MSCI Emerging Markets’ 1.22x and MSCI World’s 1.96x.

Such turbulence in the Russian financial markets and a major slowdown of the Russian economy in the aftermath of the sanctions was expected to have a significant impact on the economies with strong economic ties to Russia. Eastern European markets (including the Commonwealth of Independent States [CIS]), which have the closest links with Russia) were considered to be the most vulnerable. Russian ban on a number of imported food items and some raw materials (meat, fish and vegetables) from the countries that had imposed sanctions have also played a role. Although Western European markets tend to be relatively less linked to Russia, they were also expected to be potentially affected through their trade, energy, investment, and financial ties to Russia.

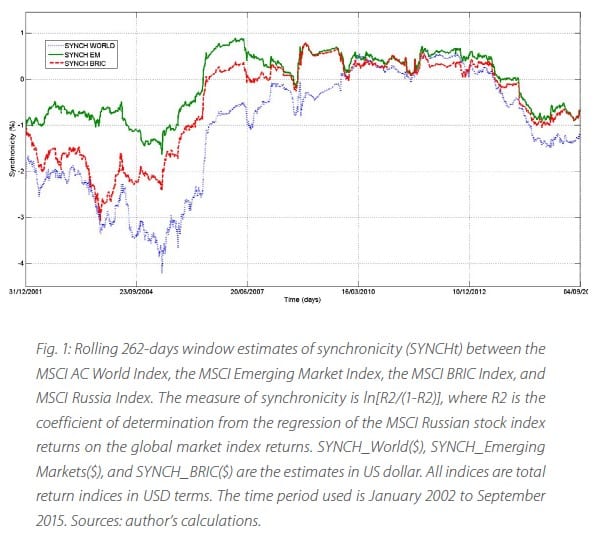

However, according to the findings of University College London-based research, in the period until the end of 2015, there is virtually no evidence of any increase in co-movement between the Russian stock market returns (that is the gain or loss in the stock market index in a particular period) and returns in countries with relatively close economic ties to Russia (only some short-term effects could be identified). In fact, the decrease in returns correlation with the Russian stock market occurred rather uniformly across developed, emerging, and frontier markets, regardless of the strength of economic links with Russia. The degree of return co-movements with foreign stock markets has declined in about 85% of cases, with the decrease in correlation ranging from 46 to 83 percent.[1] The overall degree of synchronicity of Russian and global equity market returns has also declined dramatically (see Figure 1).

The dramatic increase in synchronicity across the Russian sectoral stock indices after the sanctions were introduced, also confirmed that economic sanctions imposed on Russia effectively isolated the Russian equity market from the rest of the world and triggered widespread portfolio outflows from the market – the so-called “flight-to-quality” phenomenon frequently observed during the emerging markets crisis.

From the portfolio management perspective, while still being regarded as a major emerging market, the Russian stock market’s declining capitalization and free-float led to a radical fall in Russia’s weight in investable equity indices, such as the MSCI Emerging Markets Index. Despite the attractive valuations in the Russian equity market, the choice of available investments remained limited due to the sanctions imposed on the country. As a result, the decrease in co-movement of the Russian stock market with the rest of the world was unlikely to provide international investors with superior diversification opportunities.

The uncertainty over the sanctions ensured that the returns of the Russian market in the medium-term continued to be predominately driven by idiosyncratic news. The effect of decoupling of the Russian market from the rest of the world persisted. The strong rebound in the Russian stock market, which started in 2016, can be viewed as a response to the latest signals indicating that the geopolitical risks surrounding Russia are decreasing, and the country is showing signs of returning to growth. MSCI Russia delivered 54.82% USD returns in 2016 and the upward trend is likely to persist in 2017 amid attractive valuation ratios.

[1] See Castagneto-Gissey, G. & Nivorozhkin, E. (2017). Global equity markets decoupling from Russian during the 2014 Ukrainian crisis. Economic Analysis and Policy Vol. 54; and Castagnet-Gisey, G. & Nivorozhkin, E. (2016) Russian Stock Market in the Aftermath of the Ukrainian Crisis. Russian Journal of Economics Vol. 2.